In the worst case scenario?

A customer sues you, a fire breaks out, or a technical error cripples your business. This can not only be stressful but also costly.

Examination error

An audit error leads to inaccurate financial reports and legal consequences.

Faulty tax advice

A client asserts claims for allegedly faulty tax advice.

Data loss

Loss of confidential financial data leading to a claim for damages.

Don't worry - we have everything in sight for you.

Protection for your exams, clients, yourself, and your auditing firm.

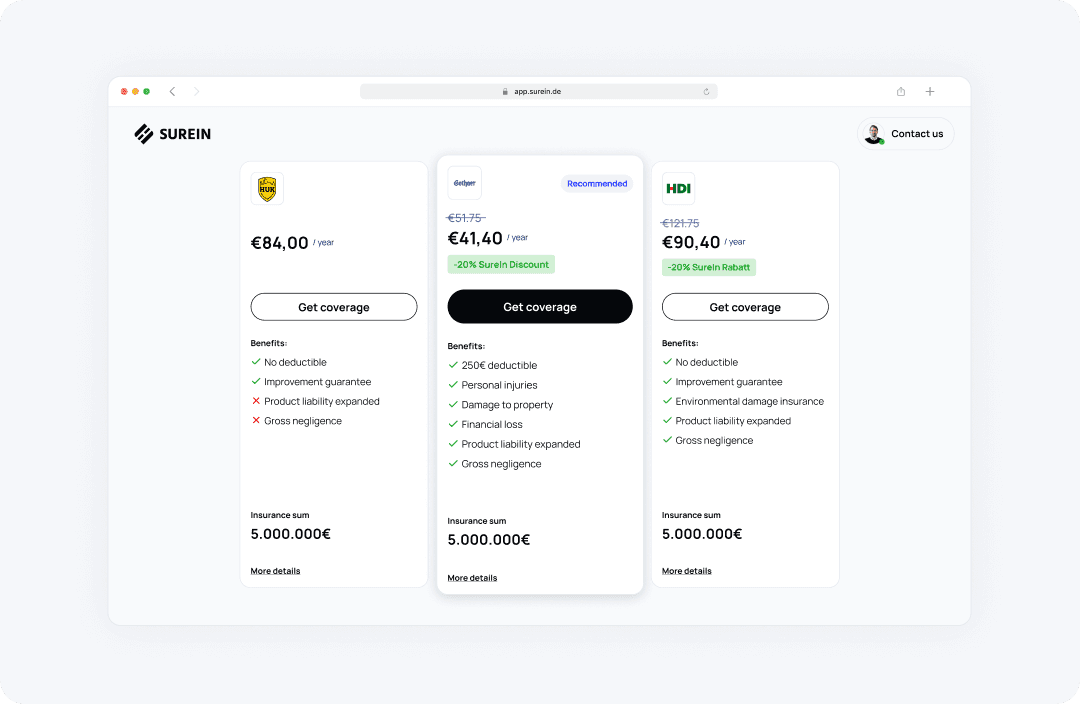

The most important commercial insurances for auditors

A customizable and 100% digital insurance management solution tailored to you.

The most important insurances for auditors

It is important for auditors to carefully review the scope and terms of their insurance to ensure they are adequately protected against the potential risks they may face.

To protect against such claims, we typically recommend the following types of insurance to auditors.

Important commercial insurances for auditors are:

Professional liability insurance

This insurance provides protection against claims due to errors, negligence, or other breaches of duty in professional practice. It usually covers the costs of legal defense and damages.

General liability insurance

This insurance provides protection against claims arising from injuries or damages occurring outside of professional practice, such as property damage or bodily injury from accidents, etc.

Assets damage liability insurance

This insurance is specifically tailored to the needs of professional groups who provide services and offer professional advice. It covers financial losses arising from errors or negligence in the provision of these services.

The right business insurance protects auditors from these types of claims:

The most common and severe insurance claims raised against auditors can be diverse, but some of the most prominent ones are:

Error or negligence in the examination

This can occur when an auditor makes mistakes or overlooks important information during an examination, which can lead to financial damages for the client.

Breach of contractual obligations

Auditors have contracts with their clients that establish certain obligations and expectations. If these obligations are not fulfilled, claims for breach of contract may arise.

Violation of professional duties

Auditors have ethical and professional standards that they must adhere to. A breach of these standards may lead to legal claims.

Violation of laws and regulations

Auditors must comply with applicable laws and regulations. Violation of these can lead to claims from clients or government authorities.

Liability to third parties

Third parties relying on the audit reports or findings could make claims if they suffer damage from the actions or omissions of the auditor.